Did Apple make your startup obsolete?

Startups, Fintech

Apple recently concluded its WWDC event for 2022, and it unveiled a whole bunch of new Apple products. Attendees also got a first look at the completely redesigned MacBook Air and the updated 13-inch MacBook Pro powered by the breakthrough M2 chip; new features coming to iOS 16, iPadOS 16, and much more. But what about the startup founders, they are usually quite interested in Apple events. Not because they want to know about the new home screen or the new ways you can share your photos but because Apple every year brings some innovation in their ecosystem which might make their startup obsolete. WWDC 2022 was no different as Apple forced the founders of a lot of companies to bitetheir nails.

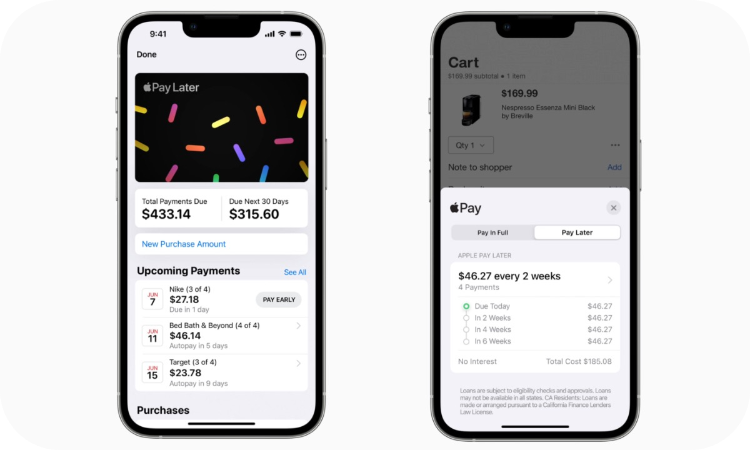

Apple Pay Later

Buy now, pay later, no interest

Have you ever got the feeling when you saw something amazing and you just have to buy it but it’s the end of the month and you don’t have enough money remaining or it’s just too expensive for you to be purchased in a single transaction. To help users make such purchases and to help merchants increase the sale of such products, some fintech players came up with a solution that is now infamously known as BNPL. So how does BNPL actually work?

You are shopping in an online store

You found a product that you really liked but it costs $1000 but you only have $500 in your bank account.

As you checkout to buy the product, you will see some options like “Pay with SomeCompany buy now pay later scheme”

Once you select such a BNPL option, these companies do a quick check of your credit score before your request is approved.

Some BNPL companies charge interest while others provide no-interest repayment for a few months, and if a payment deadline is missed then a heavy penalty is imposed quite similar to credit cards.

Once your request is approved you will have to pay a minimum amount usually 25% of the product price so in this case $250. The remaining $750 will be paid by the BNPL service provider.

Technically it is a loan (in the above situation a loan of $750) but these companies have marketed it as BNPL since loan is often associated with negative financial emotion

These BNPL companies charge a high commission from the merchant usually as high as 4-6 percent.

The other source of earning for these companies is credit default i.e. whenever a user misses a payment deadline a high-interest rate is charged (could be as high as 30%)

How are customers benefited?

Users are already registered with Apple Pay

No interest for 6 months, zero fees

Trust and security provided by Apple

How are merchants benefited?

No commission charged by apple

No extra payment method setup since more stores already accepts payment from apple pay

Startups Most Affected:

Afterpay

Klarna

Affirm

Zip

This will only affect the iPhone users of these companies and a significant number of android users might continue to use their product offerings but still, the revenue might take a serious hit. It will be interesting to see if Google comes up with a similar BNPL offering integrated with Google Pay, then these startups will have to go back to the drawing board and come up with something new.

Apple Passkeys

Have you ever used the same password twice? Guilty!

Password-only login is one of the greatest security issues over the internet, which is why most big companies today provide 2-factor authentication using either an OTP-based login or TOTP from authenticators like Google Authenticator.

Your vulnerability is increased if you are using the same password twice, leading to hackers stealing your sensitive data, information, and in some cases even money.

This became such a common problem that some companies introduced the idea of a password manager that securely stores all your passwords and allows you to login across devices seamlessly.

Do you ever feel how amazing the world would be if there were no passwords required for a website? You could just authenticate using your fingerprint or faceID and you won’t have to worry about remembering anything. Seems like we finally found a solution to this problem “Passwordless Web”.

The idea of passwordless authentication called WebAuthn is not new and was first introduced by FIDO Alliance in 2013, since then around 90% of the browsers have added support for it.

So how does Webauthn works?

Suppose you want to create an account on www.facebook.com.

When you register it will ask for your username only (no password) and your device will generate a public-private cryptographic key pair, the public key will be sent to the Facebook server while the private key will always be stored in your device.

The next time you want to login, you need to authenticate using your fingerprint or FaceID, or mobile pin and you will be authenticated

You could sign across devices using a QR-code-based solution

For a working demo check out this project website (https://webauthn.io/)

Benefits of using WebAuthn :

It is the fastest available method for authentication

Phishing attacks are not possible

It is the most secure and hassle-free method of authentication

Problems with WebAuthn

It is fairly new and cross-device authentication is still in development phase.

The digital services will need to update their code so switching to this method will not be immediate and easy

So who needs a password manager if they don’t have a password?

Startups Most Affected:

1Password

Keeper

Nordpass

Roboform

It sure seems like a long and tough journey ahead for WebAuthn but apple providing APIs and native support for it in all devices of the apple ecosystem will surely give this industry a boost.